Behind on Student Loans : As 2026 begins, millions of student loan borrowers in the United States who are behind on payments could face serious financial consequences including direct deductions from their paychecks. After years of pandemic-era relief and pauses on collections, the federal government is restarting aggressive enforcement actions aimed at defaulted federal student loans, raising fresh concerns for borrowers nationwide.

What’s Happening Now: Wage Garnishment Resumes

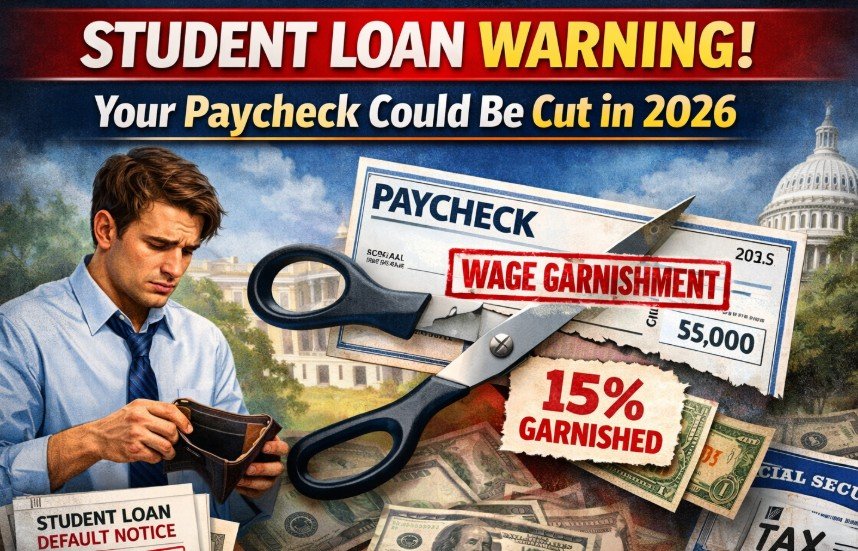

Federal student loan collections, including wage garnishment, officially resumed in early January 2026. The U.S. Department of Education has begun sending official notices to borrowers who have missed payments for more than 270 days, giving them 30 days’ notice before garnishment can begin. Once enforced, employers can be required to withhold up to 15% of a borrower’s disposable income directly from paychecks to repay defaulted loan balances.

This marks a major policy shift after the CARES Act and subsequent pandemic relief paused such actions for over five years, shielding borrowers from garnishment, tax refund seizures, and Social Security offsets.

Who Is at Risk?

• Borrowers in Default: Those who have failed to make payments for at least 270 days and have not entered repayment plans or rehabilitation.

• Millions of Borrowers: Around 5.3–5.5 million people could receive garnishment notices, with notices expanding month by month throughout 2026.

• First Wave Notices: In the first week of January, about 1,000 borrowers began receiving garnishment notices — signaling the start of a broader rollout.

What Can Happen to Your Paycheck

If garnishment begins, your employer must withhold up to 15% of your disposable income — which is your pay after legally required deductions like taxes. This money is then redirected to pay down your delinquent student loan balance. There is no requirement for a court order for federal loan garnishment, making this process faster and more automatic than many other forms of debt collection.

Other Federal Collection Actions

In addition to wage garnishment:

• Tax refund offsets and other federal benefit reductions (including Social Security) can also be used to collect defaulted loan money.

• Millions of borrowers missed payments during and after the pandemic relief period, contributing to a surge in defaults and collection risk.

What Borrowers Should Do Immediately

If you receive a garnishment notice, experts recommend taking prompt action within the 30-day window:

1. Request a Hearing: You can object to garnishment by requesting a hearing, presenting evidence such as financial hardship or errors in loan records.

2. Loan Rehabilitation: Entering an approved rehabilitation plan can help stop garnishment and remove default status (though that process takes time).

3. Loan Consolidation: Consolidating defaulted loans can quickly halt garnishment, but default may still remain on your credit report.

4. Pay or Negotiate: Paying the debt or entering a repayment agreement with your loan servicer may avoid further collections.

Policy and Political Landscape

There is ongoing legislative and political conflict around wage garnishment and student loan policy. Some lawmakers have proposed bills to suspend or limit garnishment authority and expand borrower protections, including refunding improperly garnished wages or restricting garnishment after long outstanding periods.

Additionally, federal policies governing income-driven repayment plans and forgiveness eligibility are undergoing significant changes in 2026 — potentially affecting how borrowers can manage long-term payments and defaults.

Struggling to stay current with federal student loan payments now carries a renewed threat to your take-home pay. With wage garnishment ramping up in 2026, millions of borrowers face the reality of seeing a portion of their paycheck automatically withheld — unless they act swiftly to resolve default status or challenge garnishment notices. Staying informed and engaging with loan servicers early can be critical to minimizing financial stress and credit damage as enforcement intensifies.

ALSO READ – GameStop Unveils $35 Billion Pay Plan for CEO Ryan Cohen- Performance Goals Spark Buzz